Shopify Is Eating Europe

In the Netherlands, 54% of new stores launched in 2025 chose Shopify. In France, 49%. We analyzed 324,000 new European stores to understand what's actually happening - and what it doesn't mean.

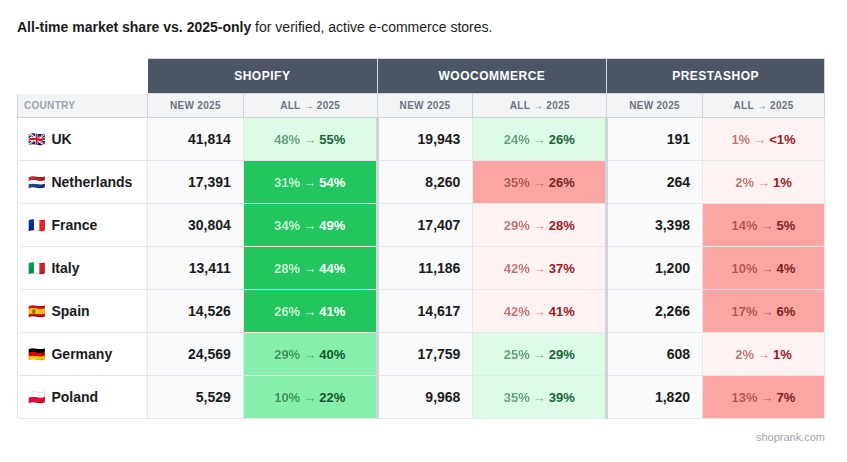

In seven major European markets, 148,044 new e-commerce stores launched on Shopify in 2025. WooCommerce got 99,140. PrestaShop got 9,747.

That's a 1.5:1 ratio. In the Netherlands, 54% of all new stores chose Shopify. In France, 49%. In Spain, 41%.

But raw store counts don't tell the whole story. We looked at what kind of stores are being created - categories, domain choices, site quality - to understand whether Shopify is actually replacing European e-commerce, or growing something new alongside it.

The shift, country by country

| Today | 2025 only | Shift | |

|---|---|---|---|

| Netherlands | 31.2% | 54.3% | +23.1pp |

| Italy | 28.3% | 44% | +15.7pp |

| Spain | 25.8% | 40.7% | +14.9pp |

| France | 34.1% | 48.8% | +14.7pp |

| Poland | 9.7% | 21.7% | +12.0pp |

| Germany | 29.1% | 40.5% | +11.4pp |

| United Kingdom | 48.1% | 54.9% | +6.8pp |

Every single European market is tilting toward Shopify. The biggest shifts: Netherlands (+23.1pp), Italy (+15.7pp), Spain (+14.9pp), France (+14.7pp).

Where the share is shifting from

The sharpest decline in new store share: PrestaShop.

| Today | 2025 only | Shift | |

|---|---|---|---|

| Spain | 17.2% | 6.4% | -10.8pp |

| France | 14.3% | 5.4% | -8.9pp |

| Poland | 13.1% | 7.2% | -5.9pp |

| Italy | 9.8% | 3.9% | -5.9pp |

| Germany | 1.6% | 1% | -0.6pp |

| United Kingdom | 0.6% | 0.3% | -0.3pp |

PrestaShop was founded in Paris. It defined Southern European e-commerce for a decade. Among stores launched in 2025, it's at 5.4% in France, 6.4% in Spain, 3.9% in Italy. That's a significant drop in share of new stores - but share of new stores isn't the whole picture. PrestaShop's installed base is large and its stores tend to be operational, local businesses that may churn at lower rates.

WooCommerce tells a more nuanced story. In the Netherlands, it dropped from 34.7% today to 25.8% among 2025-only stores (-8.9pp). In Italy, from 42.0% to 36.7% (-5.3pp). In Spain, from 42.3% to 41.0% (-1.3pp).

But WooCommerce is growing in three markets: Germany (24.7% → 29.2%, +4.5pp), Poland (35.0% → 39.2%, +4.2pp), and United Kingdom (24.0% → 26.2%, +2.2pp). These are markets where local WordPress ecosystems are strong and traditional businesses continue to choose self-hosted solutions.

But what kind of stores?

Here's where it gets interesting. Each platform attracts fundamentally different types of businesses.

Categories: lifestyle vs. traditional vs. local

| Shopify | WooCommerce | PrestaShop | |

|---|---|---|---|

| Clothing & Accessories | 32.8% | 23.1% | 30.6% |

| Health & Beauty | 19% | 16% | 10.9% |

| Food & Beverages | 6.4% | 10.1% | 8.8% |

| Home & Garden | 5.1% | 7.4% | 10.5% |

| Jewelry & Watches | 7.9% | 4.5% | 3.1% |

| Furniture & Home Decor | 3.4% | 6.4% | 4.2% |

| Electronics & Technology | 4.1% | 6.9% | 6.2% |

| Vehicles & Parts | 1.8% | 4.6% | 4.5% |

52% of new Shopify stores sell clothing or beauty products. The platform dominates DTC lifestyle - fashion brands, skincare lines, jewelry.

WooCommerce is more spread out: food & beverages (10.1%), home & garden (7.4%), furniture (6.4%), vehicles & parts (4.6%). These are traditional, often local businesses - a French cheese shop, a German hardware supplier, a Polish auto parts dealer.

PrestaShop is the surprise: 31% clothing but also 11% home & garden (2x Shopify's share). It's simultaneously fashion-heavy and deeply local - think Southern European clothing boutiques alongside hardware stores and food shops. The profile of a platform built for operational, local businesses.

Domains: global ambition vs. local roots

| Shopify | WooCommerce | PrestaShop | |

|---|---|---|---|

| .com | 48.1% | 43.4% | 27.7% |

| Country TLDs (.de, .fr, .pl...) | 39.1% | 46.5% | 61.3% |

| .store / .shop | 8.3% | 4.6% | 2.4% |

| Other | 4.4% | 5.7% | 8.6% |

Shopify stores choose global domains. 48% are on .com, another 8% on .store or .shop.

WooCommerce leans toward country TLDs (47%) but .com is close behind (43%).

PrestaShop is the most local: 61% on country TLDs. Only 28% use .com - reflecting a platform built for local, in-country businesses.

Site content: heavier vs. lighter

| Metric | Shopify | WooCommerce | PrestaShop |

|---|---|---|---|

| Median words on page | 584 | 569 | 544 |

| Median links | 47 | 58 | 66 |

WooCommerce and Shopify are surprisingly close in content volume. WooCommerce stores have more internal links - reflecting deeper product catalogs and navigation. PrestaShop stores have the most links but fewer words.

Two different dynamics

What's happening in Europe isn't one story - it's two.

Dynamic 1: New DTC brands choose Shopify. Someone in Barcelona wants to launch a clothing brand. They pick a .com domain and Shopify. This is often a net new store that might not have existed on PrestaShop or WooCommerce - the Shopify ecosystem (apps, templates, Shopify Payments) made it easy enough to try. 52% of these are fashion or beauty. Many won't survive - our survival rate data shows new stores churn at 2-3x the rate of established ones.

Dynamic 2: Traditional e-commerce continues on WooCommerce and PrestaShop. The cheese shop in Lyon, the auto parts dealer in Düsseldorf, the hardware store in Kraków - these are still choosing WooCommerce. In Germany, Poland, and the UK, WooCommerce is actually gaining share. PrestaShop's share of new stores is declining in every market - but its existing stores are the kind of local, operational businesses that tend to stick around.

The net effect: Shopify is winning the top of the funnel - dominating new store creation. But the stores it's creating look different from the ones WooCommerce and PrestaShop built their ecosystems around. And WooCommerce isn't dying - it's holding and even growing where local WordPress ecosystems are strong.

What this means

For Shopify: Europe is working. The platform is successfully exporting the DTC playbook to markets that were previously fragmented. 148K new stores in one year across seven countries is significant. The question is how many survive.

For WooCommerce: Not dead, and in three markets actually growing. Its strength is in traditional categories and local businesses that need .de or .pl domains and specific local integrations. These are real businesses that churn less. The narrative of "WooCommerce is dying" doesn't hold in the data.

For PrestaShop: New store share is down sharply - 5.4% in France, 6.4% in Spain, 3.9% in Italy, all well below installed base share. But this is one year of data, not a trend line. The installed base is large (38K stores in France alone) and PrestaShop stores tend to be local, operational businesses - exactly the kind that churn less. Lower new store share doesn't necessarily mean a shrinking platform if retention is high.

For European e-commerce broadly: The continent is consolidating around Shopify for DTC and new entrants, while maintaining a long tail of local platforms for traditional businesses. Whether this is healthy competition or premature consolidation depends on whether those 148K new Shopify stores turn into lasting businesses - or churn out within a year.

Methodology

Based on ShopRank's continuous scan of 300M+ domains. Full methodology: shoprank.com/methodology.

- Domain discovery: We monitor over 1 billion domains and discover millions of new ones every month through multiple proprietary and public sources. Every domain is scanned for technology, content, and commercial signals.

- Store verification: We count only stores that are (1) confirmed as real e-commerce businesses by our classifier - not every site running a platform plugin, (2) currently live and responding, and (3) not under construction or password-protected. This is a stricter count than raw technology detection.

- Platform detection: Identified through server headers, HTML signatures, JavaScript fingerprints, and DNS patterns. Each store is verified against multiple technical indicators.

- New stores (2025): Stores where the earliest evidence of web presence is from 2025. Estimated by cross-referencing multiple proprietary and public date sources. Stores that existed before 2025 under a different domain or platform are not counted as new.

- Country assignment: Resolved using multiple signals including domain TLD (

.de,.pl,.fr), on-page address and company information, phone number prefixes, detected courier and payment providers, and content language heuristics. Over 95% of stores have a country assigned. Stores on generic TLDs (.com,.store) are resolved using content-based signals. - Categories: Product categories classified using multilingual content analysis.

- Share shift: Difference between platform's share of all stores vs. its share of 2025-only stores. The "all stores" baseline includes only currently active stores - stores that launched earlier but went offline are not counted. Since platforms have different churn rates, this may slightly underrepresent higher-churn platforms in older cohorts.

Data and analysis by ShopRank. We scan 300M+ domains and track 8M+ verified e-commerce stores across 340+ platforms.